How Do You Buy Another House Before Selling Yours Without Losing $40K?

Read more

Low down payment and low rate home loan options for Seattle

Monday - Sunday | 8:00 am - 8:00 pm

We will never rent, sell, or misuse your data, ever.

A Division of City Mortgage Brokers, LLC

MB#2158059

This article was originally published on August 17, 2023 under the title “How Much Down Payment Do I Need to Buy a House in Seattle?” It was updated on October 01, 2025.

Buying a home always comes with a big question: How much do I need for a down payment?

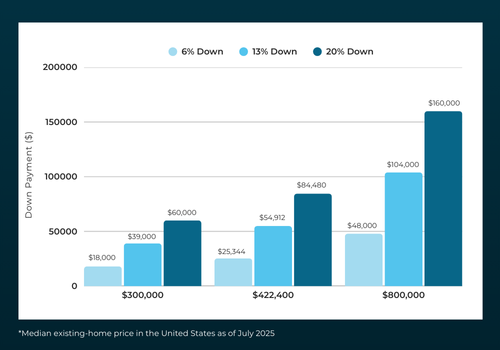

Nationally, the average down payment for first-time buyers is about 7–9% of the purchase price, while repeat buyers often put down 13–15%.

Very few actually reach the 20% mark that many people assume is required.

That’s because 20% isn’t a rule.

It’s just the number that helps you avoid private mortgage insurance (PMI) or mortgage insurance premiums, which get added to your monthly mortgage payment if you put less down.

What does that look like in real dollars?

In Seattle, where the median sale price is far higher than the national average, a $10K or even $20K down payment usually won’t go far without payment assistance programs.

This guide breaks down what buyers should know about the average downpayment of a house in Seattle. In the sections below, we’ll look at everything from loan types and payment assistance to buyer profiles and strategies that let buyers with financing stand toe-to-toe with cash offers.

Seattle homebuyers face a unique challenge.

Thanks to tech-driven demand, limited supply, and rising home prices, a down payment percentage that feels manageable elsewhere can be massive here.

For example, 10% on a $885,000 Seattle home, the average price as of August 2025, according to Redfin and Realtor.com, equals $88,500. Even a small 3–5% down payment translates into tens of thousands of dollars.

This is why local governments and state-backed payment assistance programs matter so much for qualified buyers. They help bridge the gap and make ownership possible in one of the nation’s most expensive housing markets.

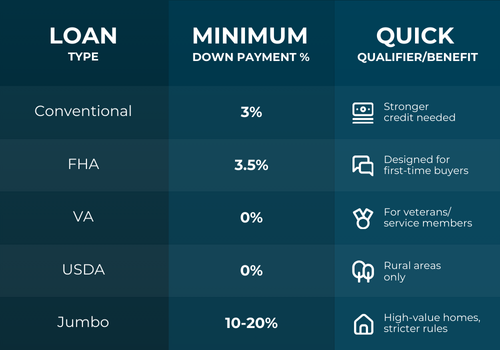

The minimum down payment you need depends on the mortgage loan you qualify for. Here are the most common programs:

These loans are flexible, are offered by many lenders, and require as little as 3% down, but they usually demand a higher credit score to qualify. For buyers with strong credit, they can mean lower monthly mortgage payments and less interest paid over time.

Backed by the Federal Housing Administration, FHA loans require just 3.5% down. Designed for first time homebuyers or those with moderate credit scores, this option remains one of the most widely used mortgage programs in Seattle.

Eligible veterans and active-duty service members can qualify for 0% down through the Department of Veterans Affairs. With no PMI required, VA loans stand out as one of the most affordable mortgage options available.

Offering 0% down for qualified buyers, these loans are backed by the United States Department of Agriculture. While they aren’t typically used inside Seattle city limits, they provide a valuable path to ownership in rural communities nearby.

High home prices in Seattle often exceed the maximum loan limits, which prevents many buyers from using a standard conforming loan and pushes them into applying for jumbo loans. These loan types require down payments of 10–20% along with stricter underwriting which means buyers need to be prepared for higher upfront costs and tougher approval standards.

While some buyers qualify for 0% options, others may need to plan for 10% or more if their home falls into jumbo loan territory.

Choosing the right loan type impacts more than the size of your down payment. It shapes your mortgage amount, determines whether you’ll pay PMI, and affects how much interest you’ll pay over time.

Understanding which path fits your situation helps you set realistic savings goals and ensures you don’t overestimate or underestimate what it takes to buy in Seattle.

I know what you’re thinking.

Considering a number like $75,000 for a down payment can make buying a home in Seattle feel completely out of reach.

You’re not alone in thinking that.

But the good news is you don’t always have to cover it on your own.

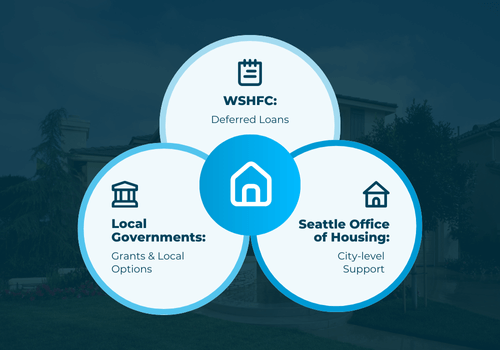

Seattle buyers have access to a range of payment assistance programs designed to reduce what you need upfront. From state-backed loans to city-level support, these programs help qualified buyers move from renting to owning.

Deferred loans from this state program can cover part of your down payment on a house.

No payments are due until the home is sold or refinanced, which means you can focus on your mortgage payments without juggling extra debt.

For many first time buyers, it’s the difference between waiting years and buying a home sooner.

City-backed programs provide support for income-qualified buyers purchasing within Seattle limits.

These programs help keep Seattle residents in the city even as home prices climb, reducing the barrier for younger buyers entering the market.

Occasionally, local governments introduce grants or special payment assistance programs to expand access to loans for first-time home buyers.

While smaller in scale than state or city options, these can combine with other programs to provide enough money to meet minimums.

In a high-cost market like Seattle, these programs can be the difference between continuing to rent and finally owning a home. By lowering upfront requirements, they make homes accessible to more qualified buyers.

When planning for a home purchase, it’s easy to focus only on the down payment.

But that’s just one piece of the financial puzzle.

Seattle buyers should also factor in several other costs that play a big role in affordability—both at closing and long after you move in:

PMI is required when you put less than 20% down. While it raises your monthly payment, it also allows you to buy years earlier instead of waiting to save a larger down payment, a tradeoff many first-time buyers find worthwhile.

Closing costs usually range from 2–5% of the purchase price. On a $600,000 home, that’s an additional $12,000–$30,000 due at closing, covering expenses such as appraisals, title fees, and lender charges.

Owning a home means being ready for the unexpected—from roof repairs to broken appliances. Keeping savings set aside can prevent those surprises from turning into financial stress.

Property taxes in Seattle vary depending on the neighborhood. These ongoing costs directly affect your monthly affordability and should be included in your overall budget from the start.

Looking at the down payment alone can create a false sense of readiness.

These additional expenses shape your real budget, and failing to plan for them can derail your purchase or add pressure after you move in. To see how all the moving pieces of a mortgage fit together—from closing costs to long-term payments—explore our free step-by-step homebuying guide.

The Bottom Line for Buyers

By budgeting for PMI, closing costs, taxes, and an emergency cushion, you’ll get a more accurate picture of what homeownership really costs. The good news: planning ahead puts you in control, helping you buy with confidence instead of stress.

Earlier we looked at national averages. Now, let’s see how different age groups and buyer types approach a down payment on a house in Seattle.

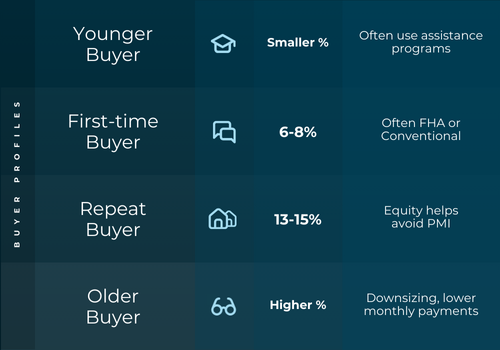

Since saving while renting in Seattle can be tough, first-time homebuyers often plan for smaller down payments, usually in the 6–8% range, with many relying on FHA or conventional programs that allow lower minimums.

By using equity from their previous home, repeat buyers tend to have more flexibility, averaging 13–15% for a down payment. This strengthens their offers and helps them avoid PMI and pay less over the life of their loan.

Retirement savings or proceeds from downsizing often fund higher down payments. This reduces the mortgage amount and provides lower monthly mortgage payments, a benefit that can be especially appealing at this stage of life.

Smaller down payments are typical of younger buyers. But while these buyers may bring the lowest median down payments, assistance programs like the FHA or state programs, help them bridge the gap and stay competitive.

Take a household earning $70,000 per year.

Depending on debt and credit score, they might qualify for a home in the $280,000–$300,000 range. A 10% down payment equals about $28,000–$30,000 upfront. That’s a stretch, but achievable with planning, equity from repeat purchases, and the right loan program.

At the end of the day, averages only tell part of the story for home buyers. Knowing where you fall helps you set realistic goals and explore the programs that can support your path to ownership without sending more money than needed.

By now, it’s clear that many Seattle buyers no longer stick to the once-standard 20% down payment. But the market is still fiercely competitive—homes sell fast, often with multiple offers.

And in that kind of environment, the more cash you can put forward upfront, the stronger your offer looks. Sellers see cash as certainty: fewer financing risks, fewer delays, fewer reasons a deal might fall apart.

This creates a challenge without a huge down payment saved: How can you stand out against offers that look more secure on paper?

The good news is that sellers don’t always choose the highest number on paper. What they want most is certainty: confidence that the deal will close smoothly and on time. That means home buyers with financing can go head-to-head with cash offers if they show they’re prepared.

To compete:

A strong pre-approval tells sellers your financing is already vetted. Full underwriting goes a step further, removing doubts about whether the mortgage loan will close.

Unlike a single bank, brokers shop multiple lenders—including private lenders—to find competitive rates and terms. This flexibility can help save you interest paid over the life of the loan and craft terms that fit both your budget and what sellers value most.

The fewer the contingencies, the stronger the offer looks. Pairing this with the ability to close fast, sometimes in as little as eight days, can outweigh a competing bid with a higher down payment.

.png)

The bottom line, home buyers don’t need a 20% down payment to be competitive in Seattle's housing market.

With the right preparation and a broker who can navigate mortgage lenders and home loans, you can build an offer that gives sellers confidence and gives you the edge without overpaying.

In Seattle, saving 20% for a down payment on a house isn’t realistic for most home buyers.

But the good news is that it isn’t required.

Across the country, people are buying homes with much less, and here in Seattle, local programs and smart loan options make ownership possible even in this high-cost market.

With the right loan, the right assistance, and the right approach, you can buy with far less than 20% down and still make a competitive offer.

Ready to find out what’s realistic for you? Start your personalized mortgage plan with Seattle’s Mortgage Broker today.

Joe Tafolla is the founder and lead mortgage broker at Seattle’s Mortgage Broker, a full-service mortgage consulting firm dedicated to helping homebuyers secure financing with competitive rates, faster closings, and personalized service.

With more than two decades in the mortgage industry, Joe has helped hundreds of families achieve homeownership.

.png)

.png)