How Do You Buy Another House Before Selling Yours Without Losing $40K?

Read more

Low down payment and low rate home loan options for Seattle

Monday - Sunday | 8:00 am - 8:00 pm

We will never rent, sell, or misuse your data, ever.

A Division of City Mortgage Brokers, LLC

MB#2158059

This article was originally published on Nov. 24, 2019 under the title “Buying a Home with Restricted Stock Units.” It was updated on September 25, 2025.

Seattle buyers face some of the steepest home prices in the country, and saving enough for a down payment can feel out of reach.

But if you work in tech or a publicly traded company, you may already have a powerful tool in your compensation package: restricted stock units (RSUs).

RSUs are a form of equity compensation that companies often include in a job offer to attract top talent, especially in competitive markets like Seattle.

When structured correctly, RSUs can serve as collateral for restricted stock loans that let you access capital without being forced to sell your shares or miss out on future gains.

For many buyers, this approach makes homeownership in Seattle possible years earlier than saving alone.

In this guide, we’ll break down how restricted stock loans work, how lenders evaluate them, the benefits and risks of using them toward a home purchase, and the key factors to consider before moving forward.

Restricted stock units are a promise from your employer to deliver shares at a later date, typically after certain conditions are met, like staying with the company or hitting performance goals.

Unlike stock options, which let you buy shares at a specified price, you don’t buy RSUs. They’re awarded to you, but you don't fully own the shares right away.

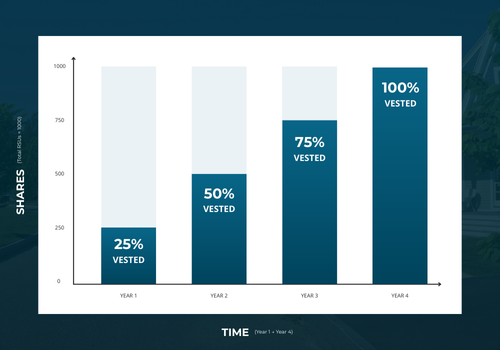

Instead, they follow a vesting schedule, a timeline that dictates when the stock becomes yours.

For example:

Until those shares vest, you can’t sell or use them as collateral. Typically, you won’t receive dividends or voting rights, either. And if you leave the company early, you may forfeit the unvested portion.

Once vested, RSUs are paid out as shares and are taxable as ordinary income. And if you later sell the stock for more than its market price at vesting, you may also owe capital gains tax.

This combination of vesting rules, taxable events, and ownership rights directly impacts how RSUs can be used for restricted stock loans, and highlights why planning is so important when using RSUs for a home purchase.

From a lender’s perspective, restricted stock loans are both an opportunity and a risk.

Because RSU values depend on your company’s stock price and market conditions, collateral value can fluctuate.

So when evaluating RSUs, lenders look at more than the stock itself.

They consider your borrower profile and factor in your credit score, income, personal loans, existing debt, and employment history to decide how much they’re willing to lend against your vested stock.

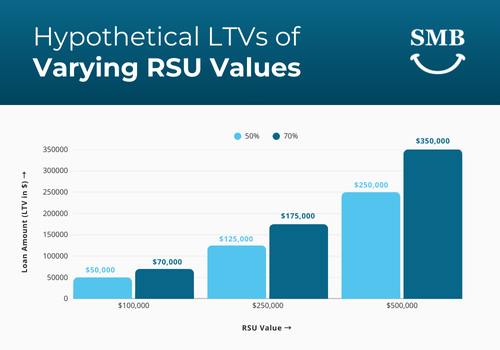

In most cases, lenders only let you borrow a percentage of the shares’ market value, known as the loan-to-value ratio (LTV).

Depending on the loan terms and your credit profile, a lender might allow you to borrow between 50% and 70% of your vested RSUs:

Some lenders may credit RSUs more favorably when qualifying borrowers for jumbo loans, which are common in Seattle's high-cost market. Though these come with stricter underwriting.

The bottom line is that most lenders consider RSUs to be a legitimate form of collateral, but they’ll put in limits and safeguards to protect themselves.

This is what makes RSUs such a powerful tool for unlocking liquidity for homebuyers.

They allow you to access capital from your holdings without immediately selling them outright, providing three important benefits for buyers in Seattle’s competitive real estate market:

Instead of waiting years to save enough cash, RSUs can be converted into financing that accelerates your timeline.

RSU-backed loans can be tailored with favorable interest rates and repayment terms, helping you balance monthly cash flow with other financial goals.

Borrowing instead of selling shares may help defer capital gains and improve long-term tax planning.

These advantages explain why Seattle buyers—especially those in the tech industry—are increasingly exploring restricted stock unit loans as a path to homeownership.

When lenders let you borrow against your vested RSUs, they typically do it through a stock loan.

These loans all follow the same basic idea we’ve described above: You pledge your vested RSUs (or other stock) as collateral to access liquidity. However, these loans can be structured in different ways depending on the lender.

If you default, the lender can only take the pledged stock. That means your house, savings, or other assets are all protected, but these loans usually come with higher rates or lower LTV ratios.

These loans can offer lower interest rates and quick access to cash, making them appealing for buyers who want flexibility and speed.

However, they’re considered a riskier choice, because if your stock value drops, the lender may demand more collateral or early repayment.

Both non-recourse and margin loan types provide a way to tap into the value of your equity compensation, but each has their own set of costs and risk.

This is why choosing the right loan structure and understanding its impact on your cash flow is critical for Seattle homebuyers.

To this point, we’ve mostly discussed the benefits of using RSUs for a down payment. And certainly, they can accelerate your path to homeownership.

However, it’s important to understand that these types of loans come with tradeoffs. Before moving forward, here are the key risks every buyer should understand:

RSU values rise and fall with your company’s stock price. A sudden drop in share price could lower the market value of your collateral and even trigger a margin call, requiring you to add more collateral or repay part of the loan balance.

Many employees already have significant wealth tied to their employer’s stock. Using those same shares as collateral magnifies that exposure, leaving you vulnerable if the company underperforms.

As explained above, non-recourse loans limit your liability but cost more. Margin loans may feel cheaper but can call your loan early if markets swing.

Only vested RSUs count as collateral. As a result, the timing of your vesting schedule plays a major role in when and how you can use restricted stock units toward a home purchase.

For some early-stage employees, regulations like 'SEC Rule 144' may limit how restricted stock is sold or pledged. While less common for buyers with publicly traded employers, it’s a reminder that compliance matters.

Understanding these risks doesn’t mean avoiding RSU-backed loans altogether. It simply means approaching them with eyes open, a solid plan, and ensuring you work with a lender who understands the risks involved with equity compensation.

RSUs are a powerful resource. But they’re only one part of your personal finance picture.

When deciding whether to use restricted stock unit loans for a home purchase, ask yourself:

1. Do the loan terms align with your income, vesting schedule, and cash flow?

2. How does leveraging stock loans affect your long-term investment strategy?

3. Are you balancing the benefits of buying a home sooner with the risks of tying even more wealth to one company?

With home prices consistently climbing year over year, these questions matter.

A well-structured restricted stock loan can help you access a home years sooner, but the right strategy balances short-term opportunity with long-term security.

In Seattle's high-cost real estate market, saving a traditional 20% down payment often means setting aside $150,000 or more.

For many renters, this is simply too large of a hurdle to overcome.

Restricted stock loans change that equation.

By using RSUs as collateral, they become more than part of your paycheck. RSUs allow you to access capital, compete in a hot market, and start building equity faster.

Of course, investing always involves risk. That’s why the right guidance is essential.

A mortgage broker who understands equity compensation can help structure loan terms, avoid early repayment surprises, and keep your strategy aligned with your financial goals.

Ready to see how your RSUs can help you buy in Seattle?

Start your personalized mortgage plan with Seattle’s Mortgage Broker today.

Joe Tafolla is the founder and lead mortgage broker at Seattle’s Mortgage Broker, a full-service mortgage consulting firm dedicated to helping homebuyers secure financing with competitive rates, faster closings, and personalized service.

With more than two decades in the mortgage industry, Joe has helped hundreds of families achieve homeownership.

.png)

.png)