How Do You Buy Another House Before Selling Yours Without Losing $40K?

Read more

Low down payment and low rate home loan options for Seattle

Monday - Sunday | 8:00 am - 8:00 pm

We will never rent, sell, or misuse your data, ever.

A Division of City Mortgage Brokers, LLC

MB#2158059

This article was originally published on July 13, 2020, with the title “Adjustable-Rate Mortgage vs. Fixed-Rate Mortgage.” It has been updated on November 29, 2025.

Choosing between a fixed rate mortgage and an adjustable rate mortgage shapes far more than the interest you pay.

It influences which homes stay within reach, how your budget behaves over time, and whether refinancing becomes part of your financial future.

In a market where mortgage rates shift quickly and buyers want confidence before committing, understanding how each mortgage rate works has never mattered more.

This guide explains the strengths and limitations of both options.

It reflects current market conditions and brings the conversation up to date with what borrowers are facing right now.

Once you see how a fixed rate mortgage compares with an adjustable rate mortgage (ARM), you’ll have a clearer sense of which path aligns with your plans.

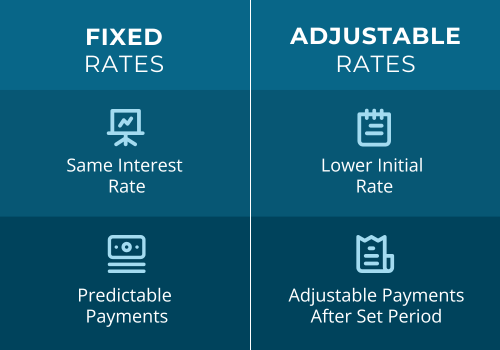

A fixed rate mortgage keeps the same interest rate for the life of the loan, whether you choose 15, 25, or 30 years. Once the rate is locked, both the monthly principal and the interest payment remain steady.

Many homeowners rely on this structure because it creates consistent expectations from the start, even as property taxes, property tax rates, and homeowners insurance fluctuate around the edges.

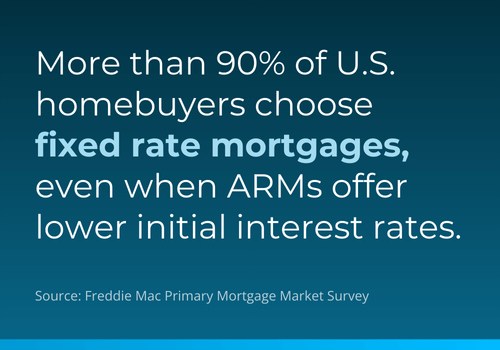

In the United States, the 30-year, fixed interest rate is almost a cultural standard.

Most lenders prefer it and most borrowers understand it because it behaves in a way that feels reliable. Other parts of the world rely far more on floating or variable loans, which gives the American model a unique sense of permanence.

A predictable payment has value.

The consistency of a fixed rate means you always know what part of your monthly payment is going toward your loan principal. You can track your progress toward full ownership. You can plan years ahead without worrying about rate adjustments creeping in later.

For many households, the stability alone justifies the cost.

A fixed rate mortgage also protects you during periods when interest rates climb. Anyone who took out a mortgage in the early 2020s felt the impact of rising rates. Borrowers with a long-term fixed loan were insulated from those jumps. The rate they secured at closing simply remained unchanged.

A steady rate comes with its own tradeoffs.

The initial pricing is usually higher than that of an ARM. Lenders typically raise the fixed rate by a small number of percentage points to balance the risk of a long-term commitment.

When interest rates decline, borrowers with fixed loans do not automatically benefit. They must refinance and take on new closing costs and fresh loan documentation.

Even with a fixed loan, not everything stays fixed. Property taxes rise, homeowners insurance responds to market swings, and HOA fees change.

Is a fixed rate mortgage easier? It can help your long-term financial planning, but it's important to remember that the surrounding costs can still move.

A fixed loan suits buyers who want clarity across the entire timeline of homeownership.

Someone settling into a forever home or someone with a tight budget often prefers the certainty that comes from predictable payments.

The value grows even stronger when the broader expectation is that interest rates will rise over the next several years. Buyers who see themselves staying in place and prefer a mortgage that behaves consistently usually find that the fixed model supports their goals.

An adjustable rate mortgage changes over time.

It begins with an initial fixed period that often lasts five, seven, or ten years. After that, the rate resets at scheduled intervals based on broader market rates. The structure can feel complex at first, although the logic behind it is straightforward.

A 5/1 ARM, for example, provides five years of stability before annual changes begin. Other versions work in similar cycles, including 7/1 and 10/6. These are known as hybrid ARM loans because of the blend of fixed and floating phases.

During the introductory period, borrowers typically receive a lower initial interest rate than they would with a long-term fixed loan.

Most ARMs limit how far the rate can move with rate caps on each adjustment and over the full loan’s term. These limits provide a buffer from extreme swings and help most borrowers understand the boundaries of potential future payments.

The most immediate benefit of an ARM is the lower initial payments that stem from the initial rate. This often unlocks a wider range of homes or creates room for savings, renovations, or other financial goals.

Buyers who expect rising income sometimes choose an ARM because the early savings support their budget at a time when cash flow matters most.

There is also a natural advantage during periods when interest rates decline. An ARM adjusts to the lower environment and reduces the monthly mortgage payment without requiring you to refinance.

The loan adapts to the market, not the other way around.

The risk of an ARM emerges once the ARM’s fixed rate period ends.

If market rates have climbed, the new payment reflects that shift.

As a result, households that expected stability or slow income growth may feel squeezed. A difficult economy can intensify the problem when declining values limit access to refinancing.

The financial strain in 2008 showed how risky an ARM can become when several forces hit at the same time. It wasn't only the interest rates that moved upward. Home values fell, and refinancing became difficult, so borrowers had fewer ways to manage rising payments.

An ARM works when you have a clear sense of timing.

If you plan to sell before the fixed rate introductory period ends, the adjustable feature may never affect you.

The same applies if refinancing is part of your long-term strategy. Buyers with rising career trajectories often prefer the early affordability. The reduced payment at the beginning creates space while they build experience, improve earnings, and settle into the property.

Comparing fixed rate vs adjustable mortgages is really an exercise in understanding your future plans.

A buyer who intends to stay in the home for decades usually benefits from the unwavering predictability of a fixed rate mortgage. Someone who expects to move within a shorter timeline or who wants more flexibility in the early years often finds that an adjustable rate mortgage offers more money saved upfront.

The right choice depends less on financial theory and more on the rhythm of your life, how long you expect to keep the property, and how comfortable you feel with change during the later years of the loan.

An ARM is not inherently a mistake. It depends entirely on your window of ownership and the outlook for your income.

Many borrowers use ARMs to reach homes that would otherwise stay out of budget. When chosen with intention, the structure supports flexibility rather than uncertainty.

Some buyers expect the overall rate environment to settle in the coming years. If that happens, the adjustable structure can work to your advantage. The early savings are real, and the potential for a smoother future refinance remains within reach.

The rates seen in 2020 and 2021 came from extraordinary circumstances.

They were not typical then, and they are even less likely to reappear in the near future.

Economists do not rule out the possibility entirely, although most believe that a return to three percent mortgage rates would require another rare global event.

A mortgage represents both a financial obligation and a long-term partnership with your own future.

Whether you choose a fixed rate mortgage, an adjustable rate mortgage, or a hybrid ARM, the decision becomes easier once you match the structure of the loan to the structure of your life.

Think about how long you expect to stay, how your income may grow, and which type of predictability gives you confidence.

The right loan is the one that supports your goals, steadies your monthly budget, and gives you room to build home equity over time. It becomes the foundation for the home you want, and the life you plan to build there.

Ready to find out what option suits your future?

Get a free mortgage quote from Seattle’s Mortgage Broker today.

Joe Tafolla is the founder and lead mortgage broker at Seattle’s Mortgage Broker, a full-service mortgage consulting firm dedicated to helping homebuyers secure financing with competitive rates, faster closings, and personalized service.

With more than two decades in the mortgage industry, Joe has helped hundreds of families achieve homeownership.

.png)

.png)